What Medicare Does NOT Pay for in Long-Term Care (2026 Guide for Families)

Many families assume Medicare pays for long-term care, but it does not cover most ongoing caregiving needs. Learn what Medicare does and does not pay for, and how families can prepare for the real costs of long-term care.

One of the biggest and most painful surprises families face in caregiving is this:

Medicare does NOT pay for most long-term care.

Many people assume that after paying into Medicare their entire lives, it will cover extended care needs as they age.

It doesn’t.

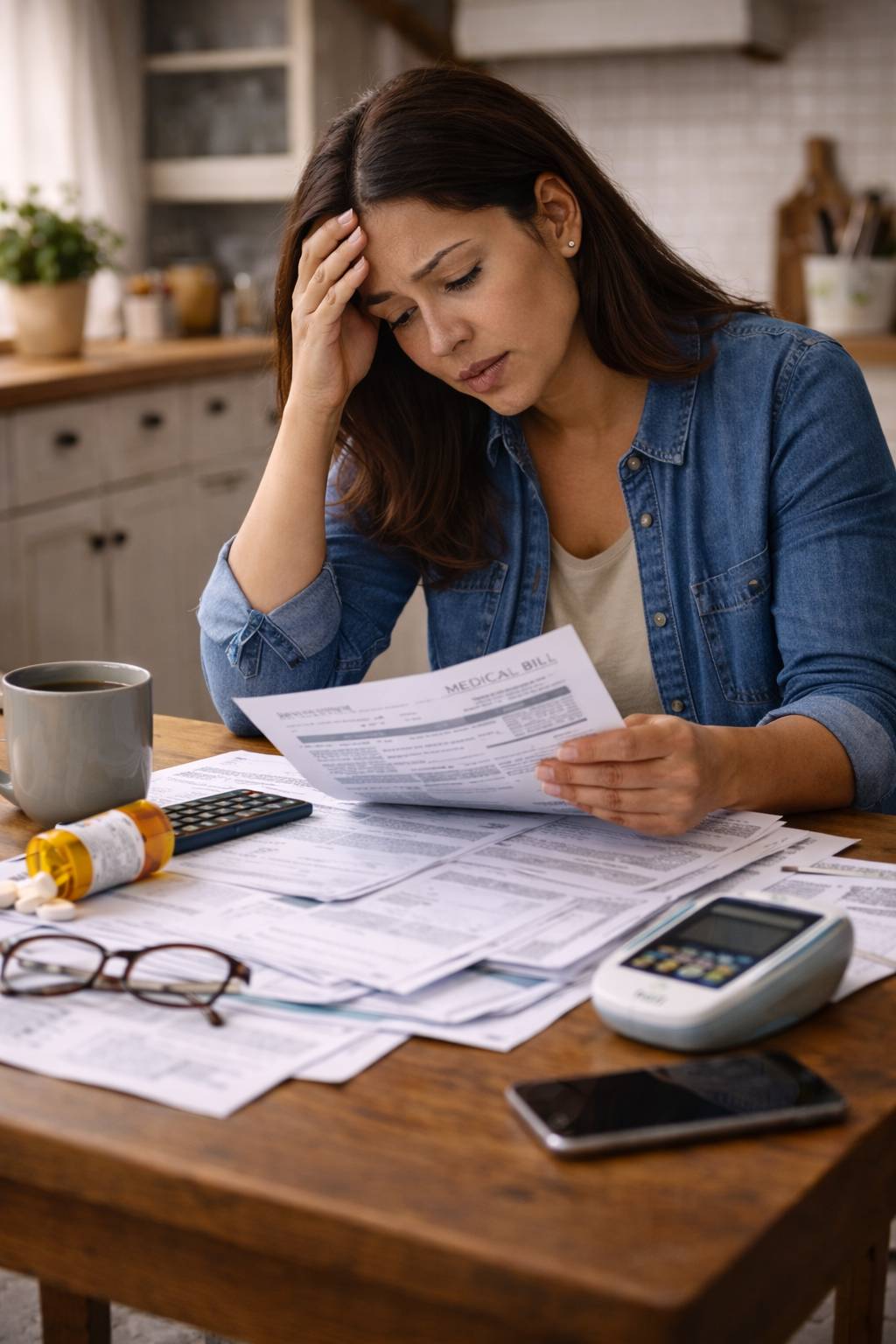

And this misunderstanding is one of the main reasons families end up overwhelmed—emotionally, physically, and financially.

If you are caring for a parent, spouse, or loved one, understanding what Medicare does not cover can protect you from crisis decisions later.

Medicare vs. Long-Term Care: What’s the Difference?

Medicare is health insurance.

It is designed to treat:

- Illness

- Injury

- Short-term recovery

It is NOT designed to provide ongoing care for daily living.

Long-term care includes help with everyday activities like:

- Bathing

- Dressing

- Eating

- Mobility

- Medication reminders

- Supervision (especially with dementia)

This type of care is called custodial care — and Medicare does not cover it.

What Medicare DOES Cover (Short-Term Only)

Medicare may pay for:

- Hospital stays

- Doctor visits

- Short-term rehabilitation

- Limited home health services

- Hospice care (under specific conditions)

But here’s the key:

👉 These benefits are temporary and medically necessary—not long-term support.

What Medicare Does NOT Pay For

1. Long-Term Nursing Home Care

This is one of the biggest myths.

Medicare does NOT pay for ongoing nursing home care.

It only covers:

- First 20 days: Fully covered

- Up to 100 days: Partial coverage

After that?

👉 You pay 100% out of pocket

Most families end up relying on:

- Private pay

- Long-term care insurance

- Medicaid (if eligible)

2. Custodial Care (Daily Help)

Medicare does NOT cover help with:

- Bathing

- Dressing

- Toileting

- Eating

- Transferring

Yet this is exactly the kind of care most older adults need.

👉 This is why family caregivers become the default care system

3. Long-Term Home Care

Many families want their loved one to stay at home.

But Medicare only covers limited, short-term home health care, such as:

- Skilled nursing visits

- Physical therapy

- Occupational therapy

It does NOT cover:

- Home care aides

- Personal care

- Ongoing supervision

👉 These services are paid privately in most cases.

4. Assisted Living

Medicare does NOT cover assisted living facilities.

These are paid through:

- Private funds

- Long-term care insurance

Costs often range from $4,000–$8,000+ per month depending on location.

5. Adult Day Care Programs

These programs provide:

- Supervision

- Activities

- Caregiver relief

But Medicare generally does NOT cover them.

The Reality: Families Become the Care System

Because Medicare doesn’t cover long-term care:

👉 Families fill the gap.

Caregivers often take on responsibilities like:

- Managing medications

- Monitoring conditions

- Coordinating appointments

- Providing hands-on care

Many do this for years, without pay or training.

Why This Is Getting Worse (And What I See Every Day)

In recent years, Medicare reimbursement changes have:

- Shortened rehab stays

- Increased early hospital discharges

- Shifted care responsibility to families

Families are often told:

👉 “Your loved one is being discharged tomorrow.”

And suddenly, they’re responsible for everything.

No training. No plan. No support.

Why You Must Plan Early

Without preparation, families face:

- Financial strain

- Burnout

- Crisis decision-making

- Family conflict

Planning ahead allows you to explore:

- Long-term care insurance

- Medicaid strategies

- Family caregiver agreements

- Structured care planning

Related Caregiver Resources

If you’re navigating caregiving decisions, these tools can help you plan ahead, reduce stress, and protect your health and finances:

👉 Explore the Caregiver Balance Guide Resources:

Helpful tools include:

- Family Caregiver Reality Checklist

- Family Caregiver Agreement Starter Guide

- Caregiver Burden Self-Assessment

- Family Meeting Planning Guide

- Emergency Preparedness Checklist

- ICE Go Bag Planning Worksheet

These are designed to help you move from reacting → planning → protecting yourself

Understanding Medicare Limits Can Protect Your Family

Many caregivers search for answers like “does Medicare cover long-term care” or “who pays for nursing home care.” The answers can prevent costly mistakes—and help you plan before a crisis begins.

Frequently Asked Questions About Medicare and Long-Term Care

Does Medicare pay for long-term care?

No. Medicare does not pay for most long-term care. It only covers short-term, medically necessary services such as rehabilitation or skilled nursing care after a hospital stay.

How long will Medicare pay for a nursing home stay?

Medicare may cover:

- The first 20 days in full

- Up to 100 days with partial coverage

After that, you are responsible for 100% of the cost.

Does Medicare pay for in-home caregivers?

No. Medicare does not cover ongoing in-home caregiving or personal care services such as bathing, dressing, or supervision.

It may cover short-term skilled care only, such as nursing or therapy.

Does Medicare cover assisted living?

No. Medicare does not cover assisted living facilities. These are typically paid for through private funds or long-term care insurance.

What is custodial care?

Custodial care includes help with daily activities like bathing, dressing, eating, and mobility.

Medicare does not cover custodial care because it is considered non-medical, even though it is essential for daily living.

Who pays for long-term care if Medicare doesn’t?

Long-term care is typically paid for through:

- Private savings

- Long-term care insurance

- Medicaid (if eligible)

- Family caregiving support

Why are hospital stays and rehab shorter now?

Changes in Medicare reimbursement have shortened hospital and rehabilitation stays.

This often results in patients being discharged sooner, with families expected to take on more care at home.

How can families prepare for long-term care costs?

Families can prepare by:

- Understanding Medicare limitations

- Exploring long-term care insurance

- Creating a caregiver plan

- Using structured caregiving tools

Final Thought

Medicare is essential—but it was never designed to carry the full weight of long-term care.

👉 Families need to understand this early

👉 Plan for it intentionally

👉 And build support before crisis hits

Because caregiving should not cost you your health, your finances, or your future.

Related Caregiver Resources

If you’re navigating caregiving decisions, these resources can help you plan ahead and reduce stress: